Under One Roof: Are Your KYC and AML Working Together or Holding You Back?

Last Revised: February 12, 2026TL;DR

KYC and AML are often treated as separate compliance tasks, but in private markets, their overlap is where most risk and inefficiency hide. Firms that handle these processes through structured data and automation gain faster onboarding, stronger oversight, and audit-ready compliance.

Know Your Customer (KYC) and Anti-Money Laundering (AML) are two core pillars of financial compliance in private markets. Though often mentioned together, they serve distinct but complementary purposes.

KYC focuses on verifying and understanding investors by collecting and validating identity information, confirming beneficial ownership, and assessing risk profiles. AML governs the ongoing detection and prevention of illicit activity, performing ongoing screening, and investigating any changes or transactions that could signal elevated risk.

KYC & AML: Two core pillars of financial compliance in private markets.

What Is the Interplay of KYC and AML?

In practice, the boundary between KYC and AML is thin — and that overlap is where inefficiencies often surface. Effective KYC lays the foundation for AML by ensuring that investor data is complete, accurate, and risk-assessed from the outset.

Accurate upfront data enables AML controls to operate effectively, reducing false positives and letting teams focus on genuine red flags.

What are Today’s KYC and AML Challenges, and How Are Firms Navigating Them?

Compliance teams today operate within a dense web of overlapping regulations — from the FATF Recommendations and successive EU AML Directives (now under the new AMLA framework), to local regulators such as the SEC, FCA, CIMA, and CSSF.

For private market firms, the challenge is magnified by multi-entity fund structures and cross-border investor bases. A single subscription may involve investors from several jurisdictions, each subject to different documentation, beneficial ownership, and reporting requirements.

How Can Firms Create Contemporary KYC Frameworks?

Designing an effective KYC framework means balancing regulatory rigor with commercial agility. In private markets, each subscription can span multiple entities, jurisdictions, and beneficial owners — making balance especially challenging

Modernizing Investor Verification

Successful firms are rethinking how they collect and verify investor data. Automated document checks, structured data capture, and digital workflows now replace manual review and email exchanges. Enhanced analytics also help uncover beneficial ownership across layered fund or trust structures — an area of particular scrutiny for regulators.

Effective KYC: balancing regulatory rigor with commercial agility.

Applying a Risk-Based Lens

A modern KYC program tiers investors by risk profile rather than treating all alike. Those with complex ownership chains, exposure to high-risk jurisdictions, or politically exposed connections, undergo enhanced due diligence. Low-risk investors follow a simplified path. This risk-based approach focuses compliance resources where they add the most value and demonstrates to regulators that the firm understands its exposure.

Managing Complex Scenarios

Edge cases remain unavoidable: politically exposed persons (PEPs), institutional investors investing through nominees, or onboarding conducted remotely. Standardized procedures and centralized data repositories reduce manual exception handling and ensure consistent treatment.

How Are Technological Advancements Changing AML Programs?

AML oversight in private markets has evolved from static, document-based reviews to dynamic, intelligence-led monitoring. As criminal networks become more sophisticated and ownership structures more opaque, compliance teams are adopting advanced technologies to identify risk patterns that traditional methods often miss.

Smarter Use of Data

The most effective AML programs no longer view investors in isolation. By capturing investor and entity information in a structured, connected format, firms can identify patterns that traditional reviews miss. For example, mapping ownership and jurisdictional links across investors helps uncover shared beneficial owners, unusual funding sources, or concentration of risk in specific regions.

AML in private markets: from static, document-based reviews to dynamic, intelligence-led monitoring.

Machine Learning in AML Detection

Machine learning is reshaping how firms assess ongoing risk. Algorithms can surface subtle patterns such as jurisdictional overlaps, recurring beneficial owners, or fund flows that diverge from typical norms. This results in sharper insight, fewer false positives, and faster escalation of suspicious cases.

Balancing Automation and Oversight

Alert thresholds and review triggers must be continuously calibrated to ensure meaningful results without overloading compliance teams. The most effective AML programs pair automation with experienced human judgment, ensuring that potential red flags are assessed with both data context and professional expertise.

The Technology Arms Race in Financial Compliance

Today, the differentiator isn’t whether firms use technology — it’s how deeply that technology is embedded into the compliance architecture itself.

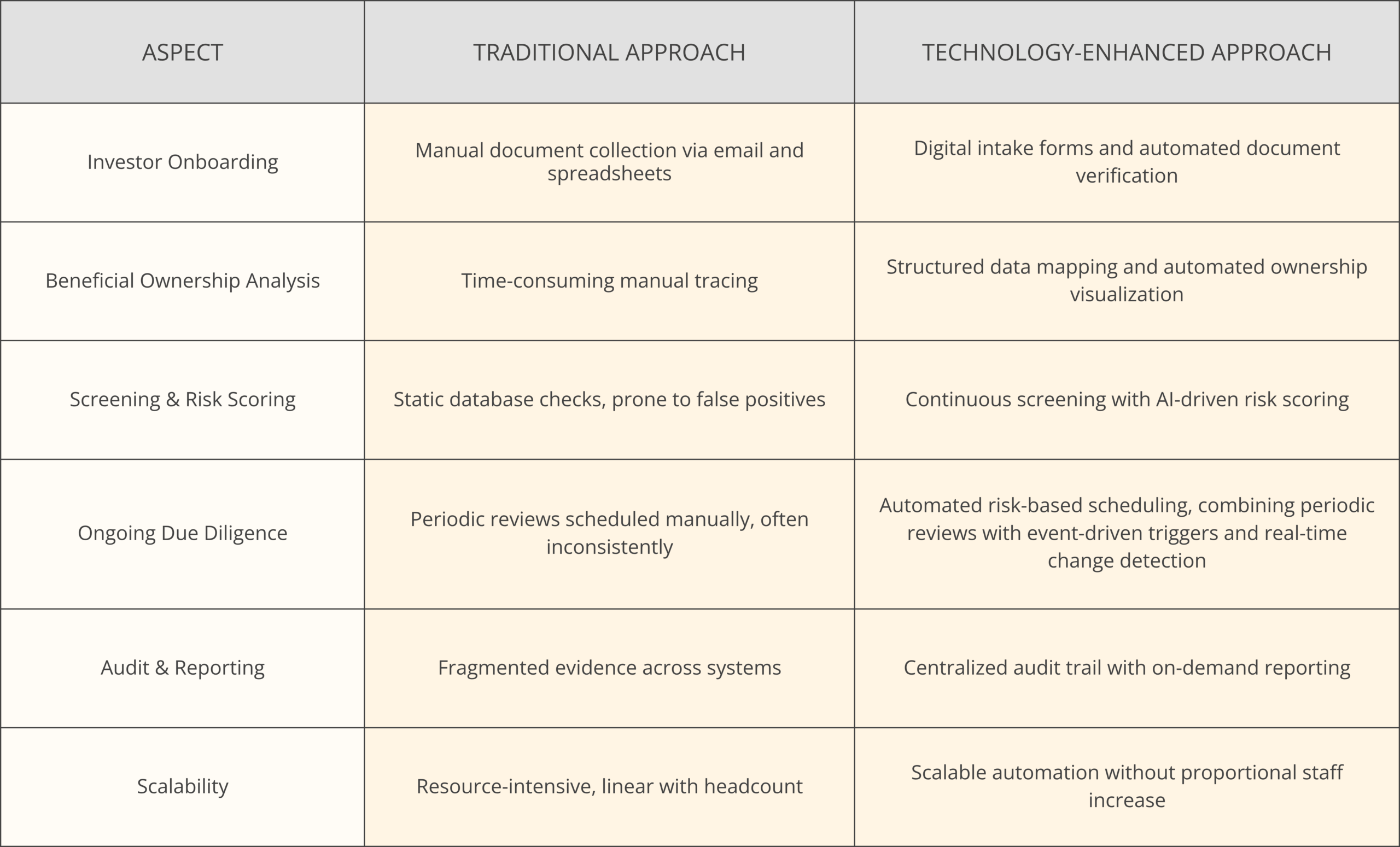

Below is a quick overview of the traditional approach compared with the modern one:

Financial Compliance in Private Markets: The Traditional Approach vs. the Tech-Enhanced Approach

The Future of Unified Private Market Compliance

The convergence of KYC and AML is redefining how private market firms approach compliance. Whether managing a hedge fund, private equity, or venture capital vehicle, regulators now expect continuous oversight across the full investor lifecycle. Meeting these expectations requires more than incremental improvements to legacy processes; it demands a unified, data-driven compliance infrastructure.

Industry-leading firms are moving away from fragmented systems and manual reviews toward integrated platforms that connect investor data and deliver real-time visibility across jurisdictions. According to a recent EY survey, over 50% of asset managers identified “efficiency through technology” as their top priority in client onboarding, However, according to that same survey, only 21% have fully automated onboarding processes — meaning that 79% still have largely manual or partially manual workflows.

The Bottom Line

Unified compliance isn’t a trend — it’s the new baseline. By connecting KYC, AML, and due diligence in one platform, firms can move faster, reduce manual load, and meet regulator expectations with confidence.

Why Blackbird?

At Blackbird, we’re built for this fast-changing reality. Blackbird’s AI-first platform unifies KYC, AML, and investor due diligence in one seamless environment — eliminating manual bottlenecks, accelerating onboarding, and strengthening assurance without added headcount

Ready to unify KYC, AML, and due diligence under one AI-first platform?

Book a demo with the Blackbird team today.

For more insights (or fun KYC memes), follow us on LinkedIn.

About the Author

Linoy Doron is a Content Strategist at Blackbird, where she translates complex fintech and compliance topics into clear, actionable insights. With a strong background in technology, SaaS, and UX, she crafts narratives that connect product value to the real needs of asset managers in the private market.